Is Tax Fraud a White Collar Crime?

By : saulcrim | Category : Criminal Defense | Comments Off on Is Tax Fraud a White Collar Crime?

8th Jan 2026

Tax fraud costs the U.S. economy billions annually, yet many people don’t understand how it differs from other financial crimes. At Law Offices of Scott B. Saul, we recognize that determining whether tax fraud qualifies as a white collar crime requires understanding both its legal definition and its real-world impact.

This guide breaks down the elements that constitute tax fraud, explains why it falls under white collar crime classification, and shows you what penalties offenders face.

What Constitutes Tax Fraud

Intent Separates Fraud from Honest Mistakes

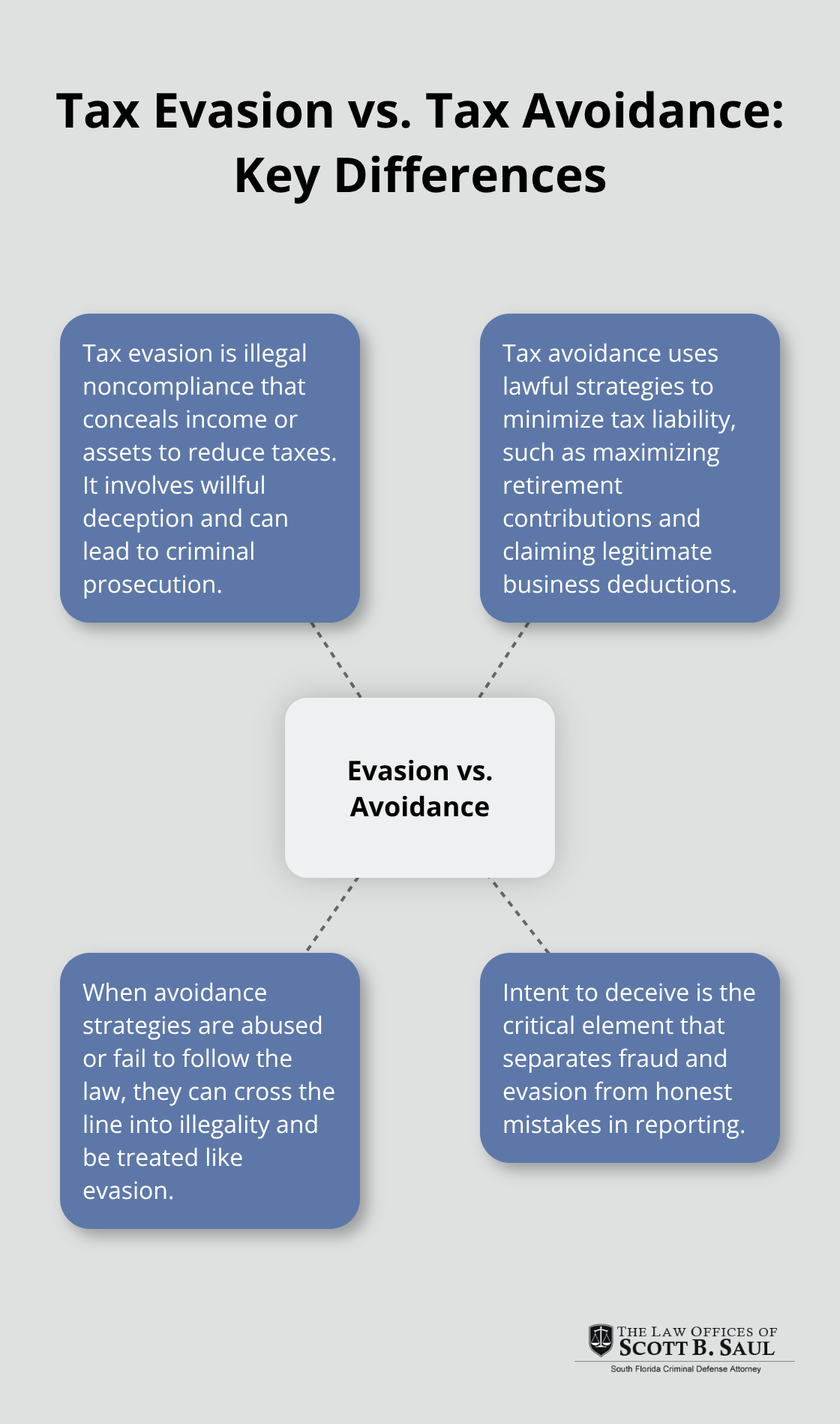

Tax fraud occurs when someone intentionally misrepresents information on a tax return to reduce what they owe. According to the Legal Information Institute at Cornell Law School, tax fraud broadly encompasses wrongly calculating asset values, misusing deductions and credits, or failing to report income at all. The defining factor is intent to deceive the IRS. Honest mistakes in reporting do not constitute fraud, but deliberate actions to deceive the IRS do. Prosecutors must prove this intentional element in court to secure a conviction.

Tax Evasion, Tax Avoidance, and the Critical Differences

The IRS distinguishes tax fraud from tax evasion, though people often use these terms interchangeably. Tax evasion is the deliberate failure to comply with tax laws, while tax avoidance uses legal methods to minimize tax liability. Tax avoidance can be illegal if a taxpayer abuses these strategies and doesn’t follow tax laws, but legitimate strategies like maximizing retirement contributions or claiming legitimate business deductions are perfectly legal. Evasion, by contrast, involves illegal concealment of income or assets.

Many people fail to recognize that underreporting cash income (including tips from service jobs) constitutes evasion and can trigger serious consequences. If unreported income gets deposited into a bank or linked to large purchases, the IRS may investigate and file charges.

Common Methods Used in Tax Fraud Cases

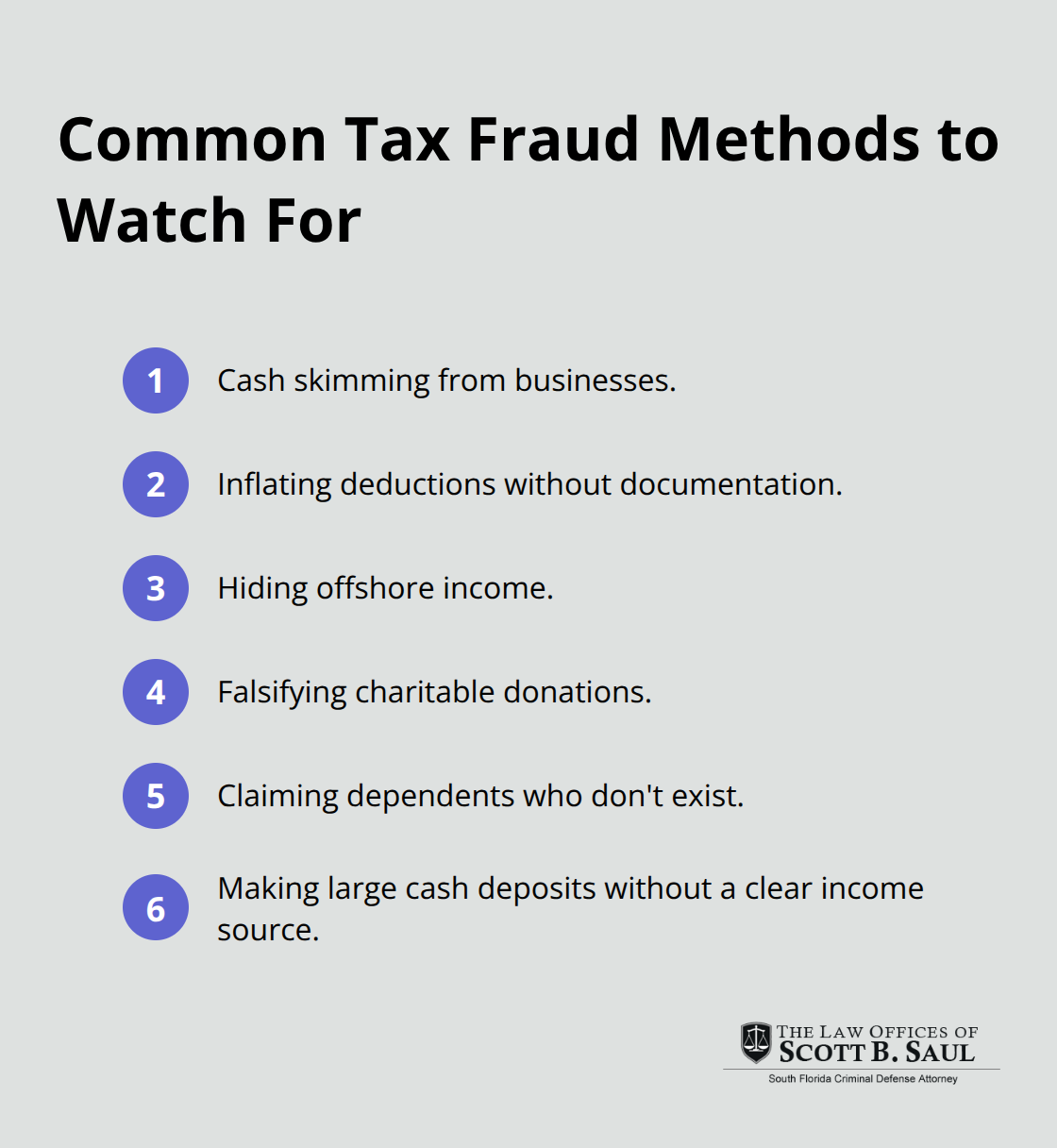

Tax fraud schemes take many forms. Cash skimming from businesses, inflating deductions without documentation, hiding offshore income, falsifying charitable donations, and claiming dependents who don’t exist all represent common methods. Large cash deposits without a clear income source signal possible tax evasion to authorities and often prompt investigation.

Prosecution data from the Transactional Records Access Clearinghouse reveals that 4,332 white-collar prosecutions occurred in 2024, with 99% targeting individuals rather than corporations. This statistic demonstrates that everyday taxpayers face real risk of prosecution. If you suspect you’ve engaged in tax evasion or face investigation, consulting a qualified attorney immediately is essential rather than attempting to handle it alone.

Why Tax Fraud Qualifies as a White Collar Crime

Tax Fraud Fits the White Collar Crime Definition

Tax fraud sits squarely within the white collar crime category because it involves financial deception committed by individuals in professional or business contexts without violence. The FBI defines white collar crime as non-violent fraud committed by business and government professionals, and tax fraud matches this definition precisely. According to the Transactional Records Access Clearinghouse, tax fraud ranks among the six most prosecuted white collar crime categories alongside financial institution fraud, federal program fraud, business fraud, health care fraud, and identity theft. In October 2024, the government reported 349 new white collar crime convictions.

Who Commits Tax Fraud and Why It Matters

What makes tax fraud distinctly a white collar crime is that it typically involves someone with access to financial records, bank accounts, or business operations who deliberately manipulates those systems to reduce tax liability. A restaurant owner skimming cash, a contractor inflating business expenses, or a professional failing to report investment income all commit white collar tax crimes. The FBI emphasizes that white collar crimes can destroy a company, wipe out a person’s life savings, cost investors billions of dollars, and erode the public’s trust in institutions, which underscores why tax fraud prosecution remains a priority despite recent enforcement declines.

Prison Time and Financial Consequences

Penalties for tax fraud convictions are severe and escalate based on the amount concealed and the defendant’s criminal history. The IRS pursues both civil and criminal penalties, with criminal prosecution reserved for willful violations involving substantial sums. Prison sentences for tax fraud convictions averaged 19 months historically, though the first half of 2025 showed median sentences rising to 14 months according to TRAC data. Beyond incarceration, convicted individuals face substantial fines, restitution to the IRS, and permanent damage to professional licenses and reputation.

Career and Asset Loss

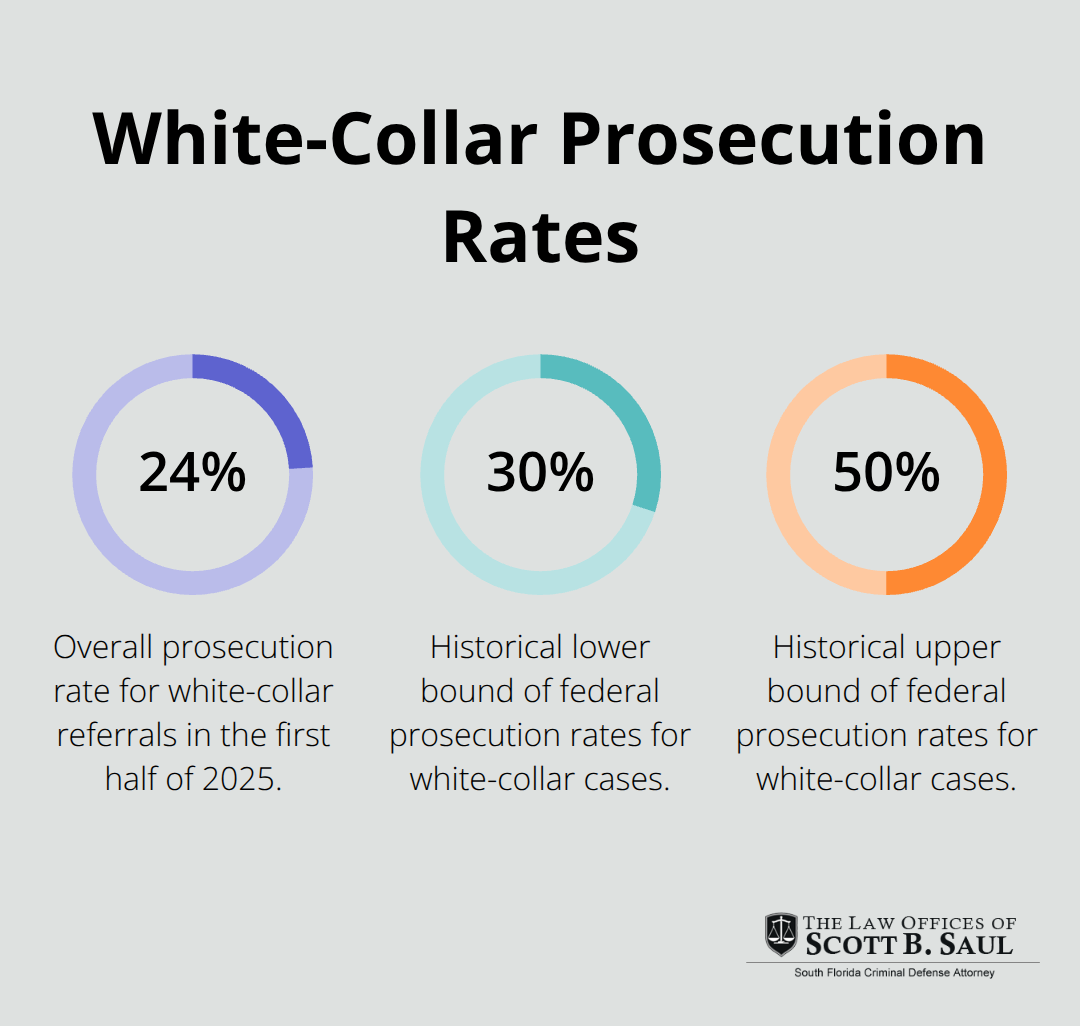

Someone convicted of tax fraud may lose their ability to work in finance, accounting, or other regulated fields, effectively ending their career. The IRS also pursues asset forfeiture, seizing bank accounts, real estate, vehicles, and other property purchased with proceeds from tax crimes. Federal prosecution rates for white collar cases have historically ranged from 30 to 50 percent, meaning the IRS takes these cases seriously when they have sufficient evidence of intent.

What Happens When You Face Investigation

If you face investigation or accusation of tax fraud, the stakes demand immediate consultation with experienced legal representation rather than attempting negotiation with the IRS alone. The complexity of federal tax law and the severity of potential penalties make professional guidance essential as you navigate what comes next.

How Many Tax Fraud Cases Actually Get Prosecuted

Prosecution Rates Tell the Real Story

Tax fraud prosecution rates reveal a critical reality that contradicts widespread assumptions about enforcement. According to the Transactional Records Access Clearinghouse, federal prosecutors filed 4,332 white-collar prosecutions in FY 2024. However, the prosecution landscape shifted dramatically in the first half of 2025, when the overall prosecution rate for white-collar referrals dropped to 24 percent compared to the historical range of 30 to 50 percent. This decline means fewer cases move forward, yet those that do still carry devastating consequences for defendants.

Who Faces Prosecution

The IRS and Department of Justice prioritize cases involving substantial sums and clear intent, meaning small underreporting incidents may face civil penalties while larger schemes trigger criminal prosecution. In 2024, 99 percent of white-collar prosecutions targeted individuals rather than corporations, demonstrating that everyday people bear the enforcement burden far more than businesses do. This disparity suggests that if you own a business or work in a professional field, the IRS views you as an accountable party rather than assuming corporate structures shield you from liability.

Sentencing Trends and Prison Time

Historical data shows that median prison sentences for tax fraud convictions are documented in federal sentencing statistics. Individuals convicted of tax fraud lose professional licenses, face asset forfeiture that strips away bank accounts and property, and encounter permanent barriers to employment in finance, accounting, law, and regulated industries.

The Full Cost of Conviction

The IRS pursues both criminal and civil penalties simultaneously, meaning you could face prosecution while also owing back taxes, interest, and substantial penalties calculated as percentages of unpaid amounts. The financial and professional destruction that follows conviction extends far beyond prison time and fines. If you face investigation or suspect your reporting may draw scrutiny, immediate consultation with experienced legal representation becomes non-negotiable, as federal tax law complexity and prosecution momentum make self-negotiation with authorities ineffective and risky.

Final Thoughts

Tax fraud is unquestionably a white collar crime, and this classification shapes how prosecutors pursue cases and what penalties defendants face. The IRS treats tax fraud with the same seriousness as other financial crimes, prosecution rates remain substantial despite recent declines, and convictions carry prison time, asset forfeiture, and permanent professional damage. Whether you underreport cash income, inflate business deductions, or conceal offshore earnings, the IRS views these actions as deliberate financial deception worthy of federal prosecution.

Accurate reporting of all income sources, thorough documentation for deductions and credits, and consultation with a tax professional when uncertain about reporting requirements all protect you from investigation. Many people underestimate how seriously authorities treat underreporting, particularly when large cash deposits or unexplained spending patterns trigger scrutiny. If you’ve already engaged in questionable reporting practices or suspect the IRS may examine your returns, addressing the problem immediately strengthens your position rather than waiting.

We at Law Offices of Scott B. Saul understand that facing tax fraud investigation or accusation demands immediate professional guidance. Contact our firm for a comprehensive consultation if you’re under investigation or facing charges. We serve clients throughout South Florida with aggressive representation designed to protect your rights and your future.

Archives

- February 2026 (5)

- January 2026 (9)

- December 2025 (9)

- November 2025 (8)

- October 2025 (8)

- September 2025 (9)

- August 2025 (8)

- July 2025 (8)

- June 2025 (9)

- May 2025 (9)

- April 2025 (8)

- March 2025 (9)

- February 2025 (8)

- January 2025 (9)

- December 2024 (10)

- November 2024 (5)

- July 2024 (2)

- June 2024 (2)

- May 2024 (2)

- April 2024 (2)

- March 2024 (2)

- February 2024 (2)

- January 2024 (2)

- December 2023 (2)

- November 2023 (2)

- October 2023 (2)

- September 2023 (2)

- August 2023 (1)

- July 2023 (2)

- June 2023 (2)

- May 2023 (2)

- April 2023 (2)

- March 2023 (2)

- February 2023 (2)

- January 2023 (2)

- December 2022 (2)

- November 2022 (2)

- October 2022 (2)

- September 2022 (2)

- August 2022 (2)

- July 2022 (2)

- June 2022 (2)

- May 2022 (2)

- April 2022 (2)

- March 2022 (2)

- February 2022 (2)

- January 2022 (2)

- December 2021 (2)

- November 2021 (2)

- October 2021 (2)

- September 2021 (2)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (2)

- April 2021 (2)

- September 2020 (5)

- July 2020 (4)

- June 2020 (4)

- May 2020 (4)

- April 2020 (5)

- March 2020 (4)

- February 2020 (4)

- January 2020 (4)

- December 2019 (1)

- November 2019 (4)

- October 2019 (4)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (4)

- April 2019 (4)

- March 2019 (4)

- February 2019 (4)

- January 2019 (4)

- December 2018 (4)

- November 2018 (5)

- October 2018 (5)

- September 2018 (4)

- August 2018 (4)

- July 2018 (7)

- June 2018 (4)

- May 2018 (4)

- April 2018 (8)

- March 2018 (4)

- February 2018 (4)

- January 2018 (4)

- November 2017 (4)

- October 2017 (4)

- September 2017 (4)

- August 2017 (7)

- July 2017 (6)

- June 2017 (4)

- May 2017 (4)

- April 2017 (4)

- March 2017 (4)

- February 2017 (7)

- January 2017 (4)

- December 2016 (7)

- November 2016 (4)

- October 2016 (4)

- September 2016 (10)

- August 2016 (4)

- July 2016 (4)

- June 2016 (4)

- May 2016 (4)

- April 2016 (4)

- March 2016 (4)

- February 2016 (7)

- January 2016 (4)

- December 2015 (5)

- November 2015 (4)

- October 2015 (7)

- September 2015 (4)

- August 2015 (4)

- July 2015 (13)

- June 2015 (9)

- May 2015 (8)

- April 2015 (6)

- March 2015 (4)

- February 2015 (4)

- January 2015 (4)

- December 2014 (4)

- November 2014 (4)

- October 2014 (4)

- September 2014 (3)

Categories

- Adjudication (1)

- Bankruptcy (1)

- Burglary Crimes (3)

- calendar call (1)

- Car Accident (1)

- Criminal Defense (395)

- Cyber Crimes (7)

- DNA (1)

- Domestic Violence (9)

- Drug Crimes (5)

- DUI (12)

- Embezzlement (1)

- Environmental Crimes (4)

- Expungement Law (2)

- Federal Sentencing Law (3)

- Firearm (3)

- Forgery (4)

- General (82)

- Healthcare (3)

- Immigration (1)

- Indentity Theft (1)

- Insurance (5)

- judicial sounding (2)

- Juvenile Crimes (4)

- Manslaughter (4)

- Money Laundering (3)

- Organized Crime (1)

- Racketeering (1)

- Reckless Driving (3)

- RICO (3)

- Sealing and Expunging (2)

- Sex Offense (1)

- Shoplifting (1)

- Suspended Driver's License (1)

- Traffic (4)

- Trending Topics (1)

- White-collar Offenses (1)