Understanding Tax Fraud Convictions

By : saulcrim | Category : Criminal Defense | Comments Off on Understanding Tax Fraud Convictions

5th Jan 2026

Tax fraud convictions carry serious consequences that can reshape your life. Federal prison time, substantial fines, and permanent criminal records are real outcomes that people face every year.

We at Law Offices of Scott B. Saul know that understanding what constitutes tax fraud and how to defend against these charges is essential. This guide breaks down the elements of tax fraud, the penalties involved, and the defense strategies available to you.

How the IRS Defines Tax Fraud

The IRS distinguishes tax fraud from simple mistakes with one critical element: willfulness. Tax fraud, per the IRS, is the willful and material submission of false statements or documents in connection with a tax return or related filing. This distinction matters enormously because a genuine error on your return does not constitute fraud, but deliberately misrepresenting your income does. The IRS separates tax evasion (willful underpayment) from tax avoidance (legal strategies to reduce your tax liability). Prosecutors must prove you acted with intent to defraud, not merely that you made a calculation error. The government bears the burden of proof, requiring clear and convincing evidence in civil cases and proof beyond a reasonable doubt in criminal cases.

When Income Reporting Becomes Fraud

Intentionally underreporting income ranks among the most common ways the IRS identifies tax fraud. This includes failing to report cash payments, tips, side income, or cryptocurrency gains. In 2024, the IRS Criminal Investigation division secured its first indictment of an individual solely for failing to report cryptocurrency earnings, where the defendant sold roughly four million dollars in Bitcoin and failed to report over six hundred fifty thousand dollars in gains on prior returns.

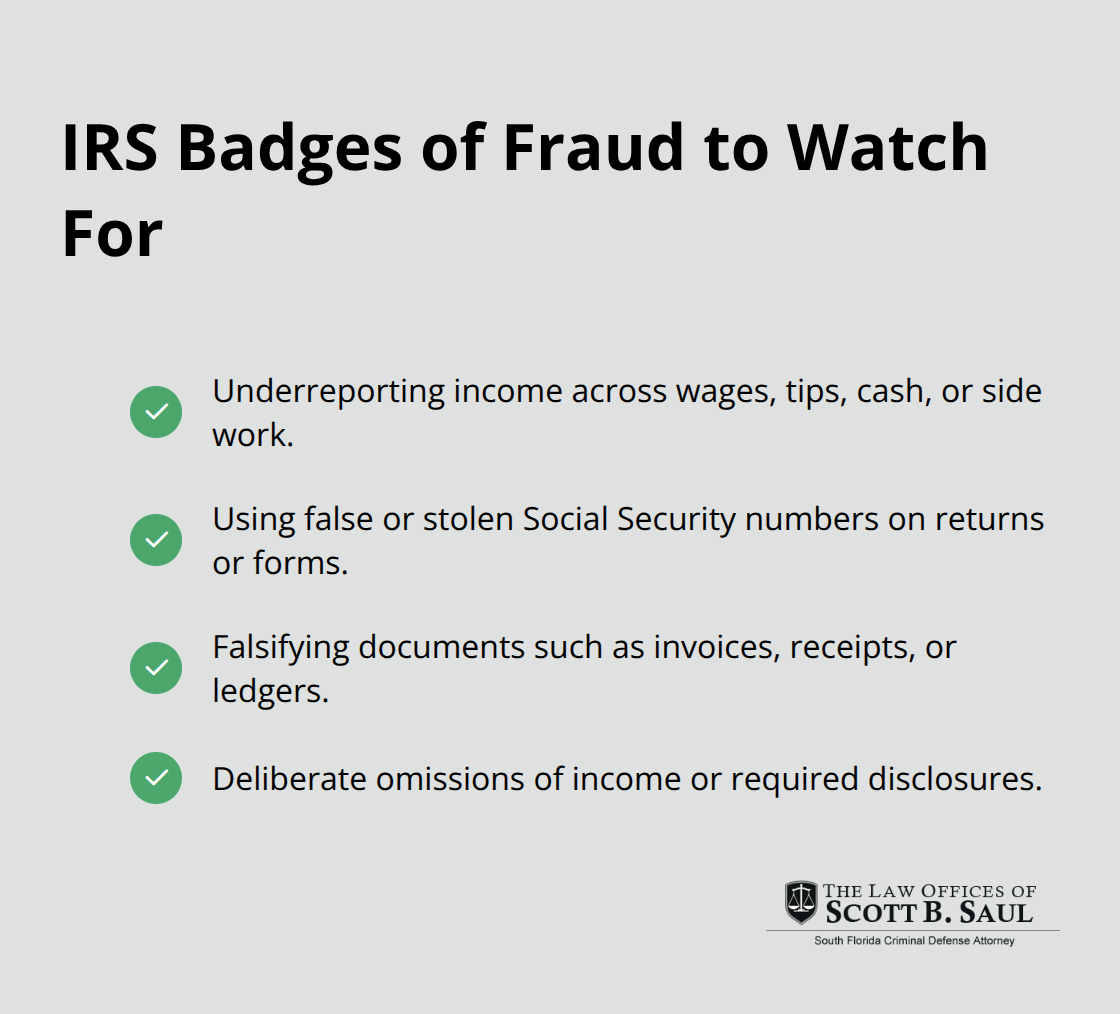

The IRS estimates that about one in six taxpayers fail to comply with tax rules, but the agency focuses its limited resources on willful violations. The badges of fraud that trigger scrutiny include underreporting income, using false Social Security numbers, falsifying documents, and deliberate omissions. Prosecutors must prove you knew the income existed and deliberately chose not to report it-simply having some unreported income does not automatically establish fraud.

False Deductions and Inflated Credits

False deductions and inflated credits represent another major avenue for fraud charges. Fabricating business losses, inflating charitable contributions, or claiming personal expenses as business deductions crosses from aggressive tax planning into criminal territory. Documentation determines the distinction. If you produce receipts, invoices, and records supporting your deductions, you have a defense. If those records are fabricated or nonexistent, you face fraud charges. The IRS scrutinizes deductions that lack proper substantiation, and prosecutors use missing documentation as evidence of intent to defraud.

Concealing Assets and Offshore Accounts

Concealment of assets and offshore accounts compounds fraud significantly. The IRS requires reporting of foreign bank accounts exceeding ten thousand dollars annually through FBAR filings and foreign asset reporting through FATCA. Deliberately hiding assets offshore to avoid taxation triggers both civil and criminal penalties. In 2024, the IRS-CI identified two billion one hundred twenty million dollars in tax fraud, with enforcement efforts increasingly targeting sophisticated schemes involving digital assets and international transfers. The IRS-CI workforce expanded to three thousand four hundred seventy-four employees (the highest level in nearly a decade), specifically to address complex cases involving hidden assets and offshore structures. This expansion signals that prosecutors now possess greater capacity to uncover and prosecute asset concealment schemes.

Consequences of Tax Fraud Convictions

Federal Prison Sentences and Substantial Fines

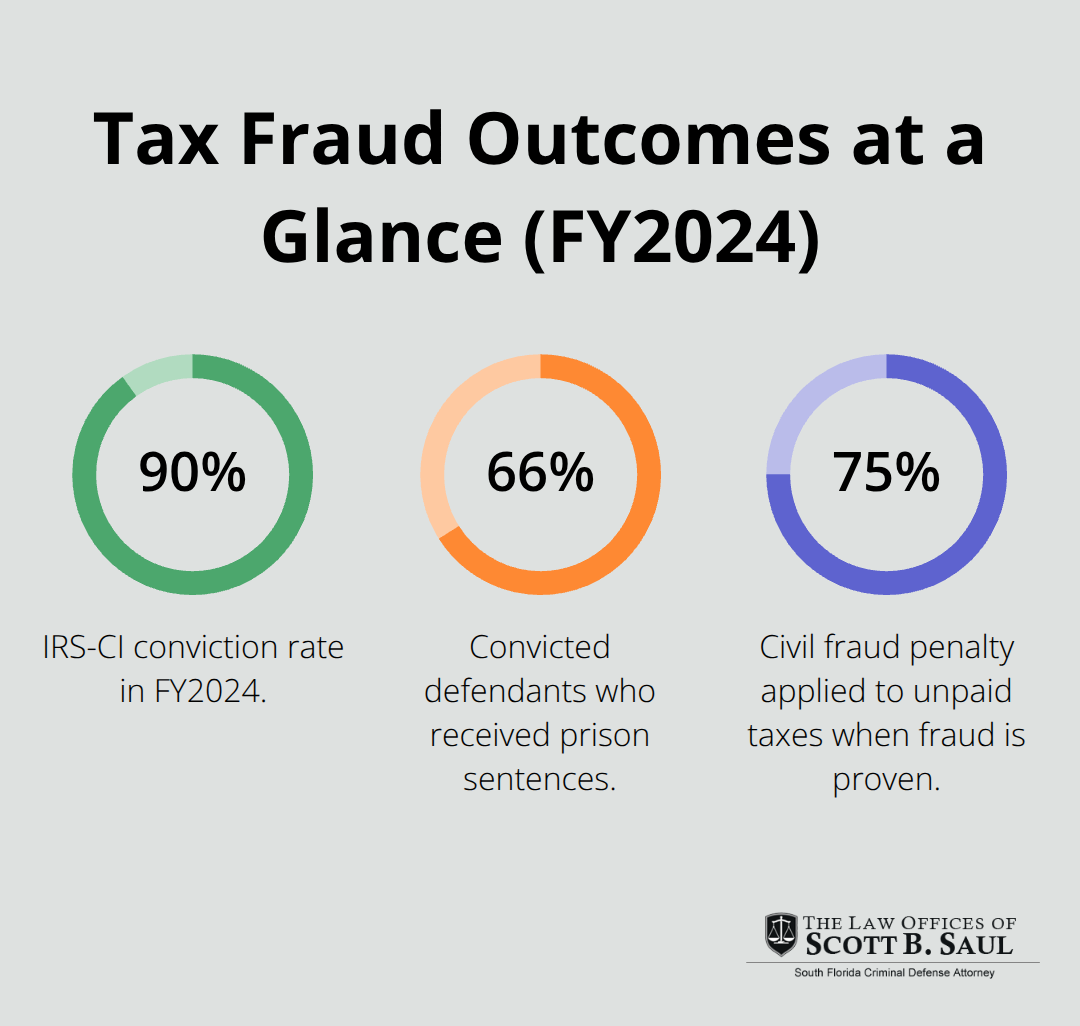

Tax fraud convictions land people in federal prison with startling regularity. In fiscal year 2024, the IRS Criminal Investigation division secured 1,571 convictions with a 90 percent conviction rate, and 66 percent of those convicted received prison sentences. The average sentence length was 15 months, though significant variation exists across cases. Defendants convicted under tax evasion statutes face up to five years in federal prison and fines reaching one hundred thousand dollars for individuals or five hundred thousand dollars for corporations.

Civil fraud penalties add another layer: the IRS imposes 75 percent penalties on unpaid taxes when fraud is proven through clear and convincing evidence. A defendant with two hundred thousand dollars in unpaid taxes faces one hundred fifty thousand dollars in civil penalties alone, stacked on top of criminal fines and restitution. The median monetary loss in tax fraud cases reached four hundred ninety-one thousand three hundred two dollars according to United States Sentencing Commission data from fiscal years 2020 through 2024.

How Cooperation Affects Your Sentence

One critical detail separates those receiving lighter sentences from those serving years: 45.2 percent of defendants received sentences below guideline minimums, typically through substantial assistance departures or downward variances. This means cooperation and early intervention matter enormously. Defendants who work with prosecutors before indictment often secure plea agreements that reduce their exposure significantly. Those who wait until trial faces harsher outcomes because judges view cooperation as a sign of genuine remorse and acceptance of responsibility.

Employment and Professional License Consequences

A tax fraud conviction creates permanent employment obstacles that extend far beyond your sentence. Employers conducting background checks see a federal conviction, and many industries automatically disqualify applicants with tax crimes on their records. Financial services, government contracting, and positions requiring security clearances become permanently closed. Professional licenses in accounting, law, and real estate face suspension or revocation following a conviction. The conviction appears on background checks indefinitely, unlike some state crimes that allow expungement after set periods. Licensing boards treat tax fraud as evidence of dishonesty-the precise quality they cannot tolerate in fiduciaries. The data shows that 86.8 percent of tax fraud defendants had little or no prior criminal history according to the U.S. Sentencing Commission, meaning first-time offenders face these same collateral consequences as career criminals.

Housing, Restitution, and Long-Term Financial Obligations

Beyond employment, housing becomes difficult. Landlords regularly reject applicants with felony convictions, and federal housing assistance becomes unavailable. This creates a cascading effect where the person loses income stability, housing security, and future earning potential simultaneously. Restitution requirements often exceed the original unpaid taxes. Courts order defendants to repay the government’s prosecution costs, investigative expenses, and the full amount of taxes owed plus interest and penalties. These obligations frequently total hundreds of thousands of dollars and continue for years or decades through wage garnishment and asset seizure. The financial burden extends well beyond the courtroom sentence.

What Happens Next in Your Defense

Understanding these consequences underscores why mounting an effective defense strategy matters from day one. The penalties you face depend heavily on how you respond to investigation and charges.

How to Build a Winning Defense Against Tax Fraud Charges

The moment you face tax fraud allegations, your instinct might be to gather documents and prepare for trial. That instinct is wrong. The IRS Criminal Investigation division convicted 1,571 defendants in fiscal year 2024 with a 90 percent conviction rate, but this statistic masks a critical reality: 45.2 percent of those convicted received sentences below guideline minimums. The difference between those who served years and those who served months often came down to timing and strategy.

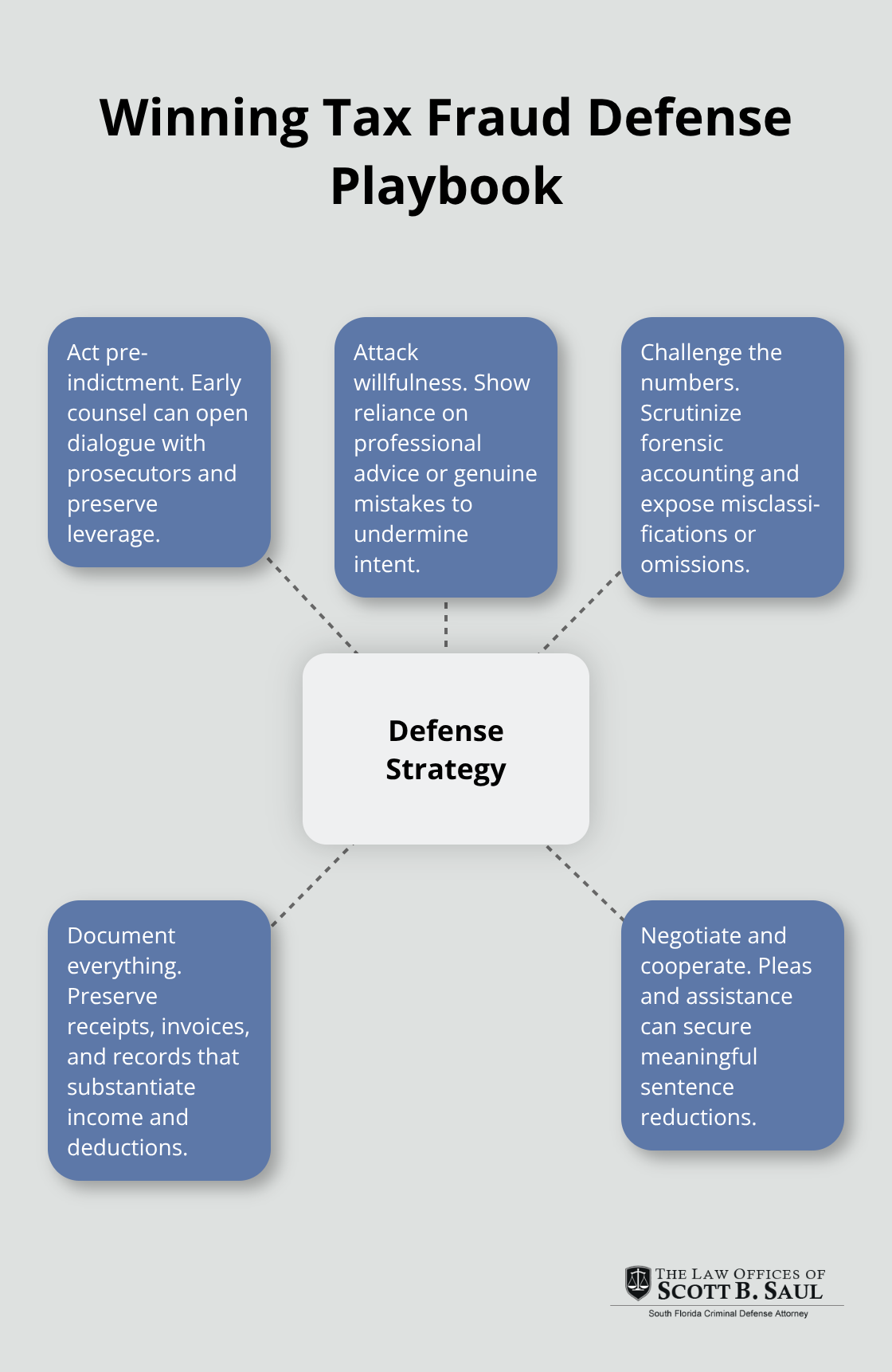

Act Before Indictment

Prosecutors distinguish between defendants who move quickly to challenge the government’s case and those who wait passively. If you face investigation, hire an experienced federal criminal defense attorney immediately-before the IRS files charges. At this pre-indictment stage, you retain leverage that evaporates after formal charges. An attorney can file protective documents, request meetings with prosecutors, and explore whether the government actually possesses sufficient evidence of willfulness.

Willfulness remains the linchpin of every tax fraud case. The prosecution must prove you knew about the unpaid taxes and deliberately chose not to report income or claim false deductions. A genuine mistake, even a substantial one, does not constitute fraud. This distinction creates your first defensive avenue. If your tax return errors stem from reliance on a CPA or tax preparer’s advice, documentation of that reliance weakens the government’s willfulness argument significantly. The IRS-CI expanded its workforce to 3,474 employees in 2024, which means prosecutors prioritize cases with clear evidence of intent. Weak willfulness evidence becomes your leverage point in negotiations.

Challenge the Financial Records

Challenging financial records accuracy represents your second major defense angle, but it requires meticulous work before trial. The government’s case often rests on forensic accounting that you must scrutinize thoroughly. Did prosecutors properly account for business expenses you actually incurred? Did they mischaracterize personal expenses as fraudulent when reasonable people could classify them differently?

Request all underlying documents the prosecution used to calculate alleged losses-bank statements, business records, correspondence with accountants. Inconsistencies in their analysis create reasonable doubt. Simultaneously, preserve all original records that demonstrate your legitimate deductions and income reporting. The United States Sentencing Commission data shows that defendants with substantial assistance departures received average sentence reductions of 51.4 percent.

Negotiate Rather Than Fight

This cooperation typically involves guilty pleas paired with honest discussions about what actually occurred. If your case involves genuine errors mixed with intentional conduct, prosecutors may accept a plea to a lesser charge in exchange for your cooperation and guilty plea. This negotiated resolution avoids trial risk entirely.

Many defendants assume trial offers their best outcome. It rarely does. Trials mean the government presents its full forensic analysis to a jury, and conviction rates in tax cases run extraordinarily high. A negotiated settlement, by contrast, allows you to control the narrative, admit responsibility on specific counts, and receive credit for acceptance of responsibility in sentencing. Courts regularly reduce sentences by 10 to 25 percent for defendants who plead guilty and demonstrate genuine remorse. The practical calculus favors resolution in most cases unless the government’s willfulness evidence is genuinely weak.

Final Thoughts

Tax fraud convictions result from willful misrepresentation of income, false deductions, and asset concealment. The penalties hit hard: federal prison sentences averaging 15 months, civil penalties reaching 75 percent of unpaid taxes, and permanent employment obstacles that follow you indefinitely. The IRS Criminal Investigation division convicted 1,571 defendants in fiscal year 2024, yet 45.2 percent received sentences below guideline minimums through early intervention and cooperation.

Prosecutors must prove willfulness beyond a reasonable doubt in criminal cases, which creates your first defensive opportunity. If your tax return errors resulted from reliance on professional advice or reasonable interpretation of complex tax rules, that documentation weakens the government’s case significantly. The timing of your response matters more than almost any other factor-waiting until formal charges arrive eliminates your leverage and forces you into reactive defense rather than proactive negotiation.

We at Law Offices of Scott B. Saul bring prosecutorial experience and over 30 years of trial work to your defense. Contact us immediately if you face tax fraud allegations, and we will position you for the strongest possible outcome in South Florida.

Archives

- February 2026 (5)

- January 2026 (9)

- December 2025 (9)

- November 2025 (8)

- October 2025 (8)

- September 2025 (9)

- August 2025 (8)

- July 2025 (8)

- June 2025 (9)

- May 2025 (9)

- April 2025 (8)

- March 2025 (9)

- February 2025 (8)

- January 2025 (9)

- December 2024 (10)

- November 2024 (5)

- July 2024 (2)

- June 2024 (2)

- May 2024 (2)

- April 2024 (2)

- March 2024 (2)

- February 2024 (2)

- January 2024 (2)

- December 2023 (2)

- November 2023 (2)

- October 2023 (2)

- September 2023 (2)

- August 2023 (1)

- July 2023 (2)

- June 2023 (2)

- May 2023 (2)

- April 2023 (2)

- March 2023 (2)

- February 2023 (2)

- January 2023 (2)

- December 2022 (2)

- November 2022 (2)

- October 2022 (2)

- September 2022 (2)

- August 2022 (2)

- July 2022 (2)

- June 2022 (2)

- May 2022 (2)

- April 2022 (2)

- March 2022 (2)

- February 2022 (2)

- January 2022 (2)

- December 2021 (2)

- November 2021 (2)

- October 2021 (2)

- September 2021 (2)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (2)

- April 2021 (2)

- September 2020 (5)

- July 2020 (4)

- June 2020 (4)

- May 2020 (4)

- April 2020 (5)

- March 2020 (4)

- February 2020 (4)

- January 2020 (4)

- December 2019 (1)

- November 2019 (4)

- October 2019 (4)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (4)

- April 2019 (4)

- March 2019 (4)

- February 2019 (4)

- January 2019 (4)

- December 2018 (4)

- November 2018 (5)

- October 2018 (5)

- September 2018 (4)

- August 2018 (4)

- July 2018 (7)

- June 2018 (4)

- May 2018 (4)

- April 2018 (8)

- March 2018 (4)

- February 2018 (4)

- January 2018 (4)

- November 2017 (4)

- October 2017 (4)

- September 2017 (4)

- August 2017 (7)

- July 2017 (6)

- June 2017 (4)

- May 2017 (4)

- April 2017 (4)

- March 2017 (4)

- February 2017 (7)

- January 2017 (4)

- December 2016 (7)

- November 2016 (4)

- October 2016 (4)

- September 2016 (10)

- August 2016 (4)

- July 2016 (4)

- June 2016 (4)

- May 2016 (4)

- April 2016 (4)

- March 2016 (4)

- February 2016 (7)

- January 2016 (4)

- December 2015 (5)

- November 2015 (4)

- October 2015 (7)

- September 2015 (4)

- August 2015 (4)

- July 2015 (13)

- June 2015 (9)

- May 2015 (8)

- April 2015 (6)

- March 2015 (4)

- February 2015 (4)

- January 2015 (4)

- December 2014 (4)

- November 2014 (4)

- October 2014 (4)

- September 2014 (3)

Categories

- Adjudication (1)

- Bankruptcy (1)

- Burglary Crimes (3)

- calendar call (1)

- Car Accident (1)

- Criminal Defense (395)

- Cyber Crimes (7)

- DNA (1)

- Domestic Violence (9)

- Drug Crimes (5)

- DUI (12)

- Embezzlement (1)

- Environmental Crimes (4)

- Expungement Law (2)

- Federal Sentencing Law (3)

- Firearm (3)

- Forgery (4)

- General (82)

- Healthcare (3)

- Immigration (1)

- Indentity Theft (1)

- Insurance (5)

- judicial sounding (2)

- Juvenile Crimes (4)

- Manslaughter (4)

- Money Laundering (3)

- Organized Crime (1)

- Racketeering (1)

- Reckless Driving (3)

- RICO (3)

- Sealing and Expunging (2)

- Sex Offense (1)

- Shoplifting (1)

- Suspended Driver's License (1)

- Traffic (4)

- Trending Topics (1)

- White-collar Offenses (1)