How to Identify Civil Tax Fraud

By : saulcrim | Category : Criminal Defense | Comments Off on How to Identify Civil Tax Fraud

29th Jan 2026

Civil tax fraud costs the government billions annually, and spotting it early matters. At Law Offices of Scott B. Saul, we’ve seen how small red flags often signal larger problems.

This guide walks you through the warning signs, common schemes, and detection methods the IRS uses. You’ll learn what to watch for and how to report suspected fraud.

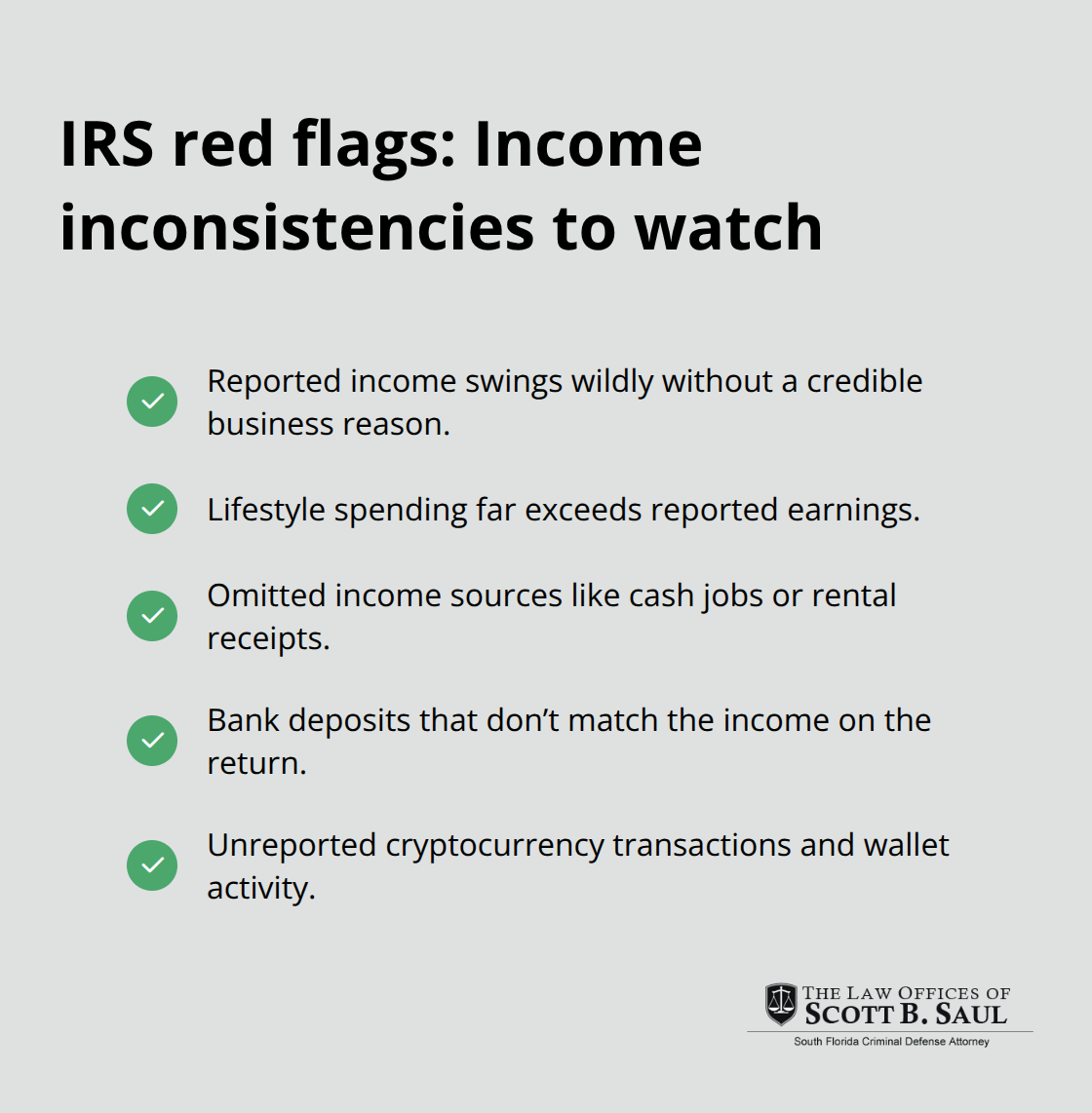

What the IRS Actually Looks For

The IRS doesn’t hunt for fraud randomly. According to the IRS Fraud Handbook, investigators apply specific indicators to spot civil tax fraud, and these patterns repeat across cases. Income inconsistencies top the list. When someone reports vastly different income year to year without business explanation, or when their lifestyle doesn’t match reported earnings, the IRS takes notice. A person driving a luxury vehicle, maintaining multiple properties, and taking expensive vacations while reporting $40,000 in annual income signals problems immediately. The IRS also flags omitted income sources entirely, missing bank deposits, and unreported cryptocurrency transactions. From 2022 to 2024, Bank Secrecy Act reporting helped uncover $21.1 billion in tax fraud, with about 87% of criminal investigations involving these reports. This means the IRS has access to financial data you might think stays private.

Deduction Red Flags That Trigger Scrutiny

Deductions require documentation, and fabricated ones leave traces. The IRS watches for deductions that exceed industry norms, personal expenses claimed as business costs, and inflated charitable donations without receipts. Someone claiming $150,000 in home office expenses when their entire business generates $200,000 in revenue invites scrutiny. False dependent claims and bogus education credits appear frequently in fraud cases.

Hidden Assets and Concealment Tactics

Hidden assets create another major problem. Accounts held in relatives’ names, offshore holdings not reported on required forms like FBAR or FATCA filings, and sudden asset transfers before an audit begins all trigger investigation. The IRS specifically examines whether taxpayers maintain multiple sets of books, alter documents, or destroy records when questioned. These actions alone demonstrate intent to conceal, which is central to proving civil fraud.

Documentation Patterns That Expose Fraud

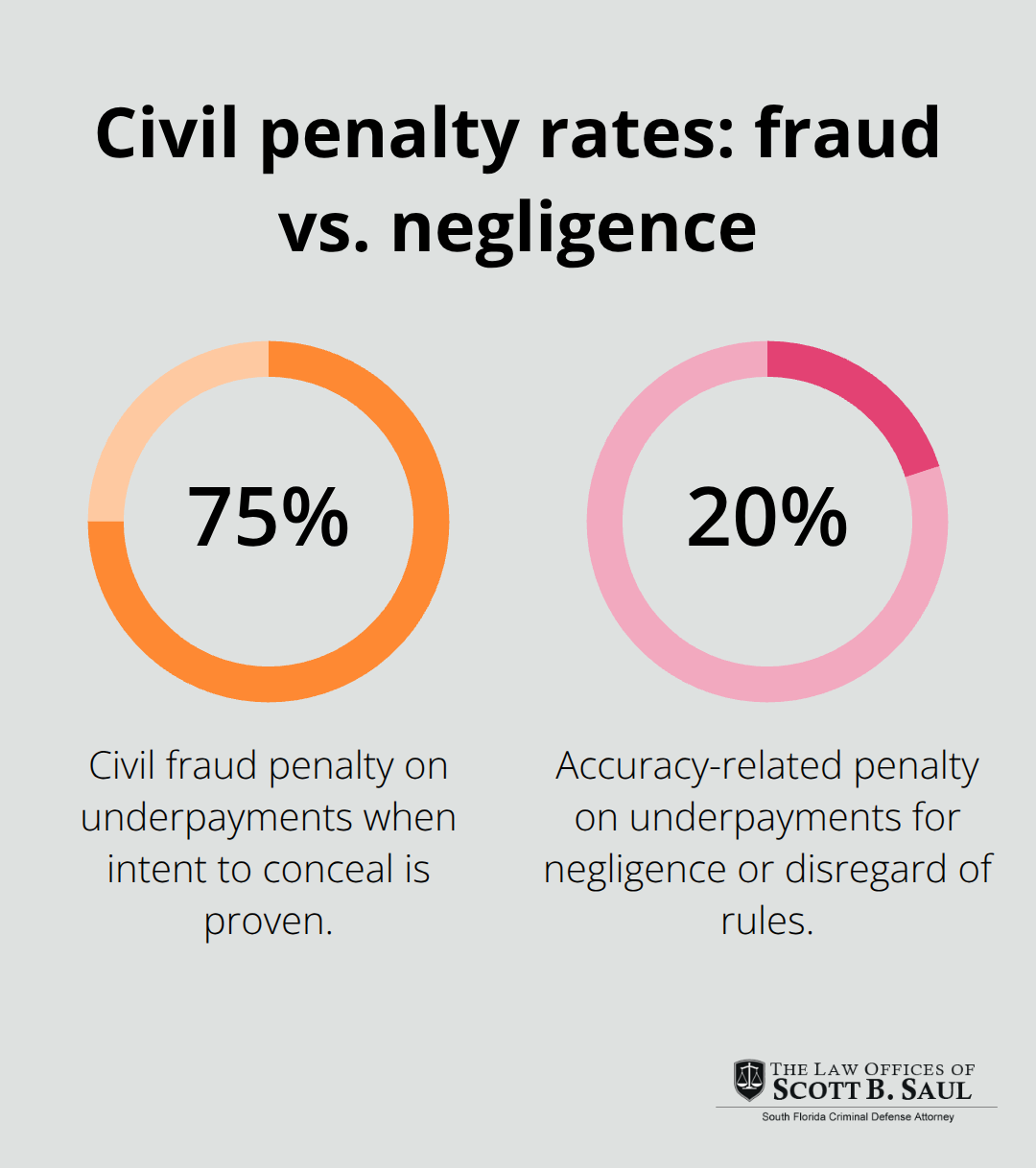

Documentation matters enormously here. Poor recordkeeping, irregular invoice numbering, and checks endorsed back to the business from third parties all constitute badges of fraud in IRS terminology. The standard for civil fraud requires clear and convincing evidence, not proof beyond reasonable doubt like criminal cases, making circumstantial evidence sufficient to establish liability and impose the 75% fraud penalty on underpayments. These same documentation failures often appear in employment tax schemes, where employers underreport workers or pay employees in cash to avoid withholding obligations entirely.

How Fraudsters Hide Income and Inflate Deductions

Underreporting Income Across Multiple Sources

Income underreporting across multiple sources remains the most common civil tax fraud tactic the IRS encounters. Fraudsters omit cash payments from side businesses, fail to disclose rental income, or hide cryptocurrency gains entirely. The IRS Fraud Handbook identifies omitted income sources as a primary badge of fraud, and the agency’s data systems catch these gaps constantly. When someone operates a consulting business generating $80,000 annually but reports only $30,000, or maintains rental properties without declaring that income stream, investigators immediately flag the pattern.

Employment tax fraud follows a similar playbook. Employers underreport workers, pay employees in cash off the books, or misclassify workers as independent contractors to avoid withholding taxes. These schemes expose businesses to criminal liability and restitution demands. The IRS distinguishes between simple errors and intentional concealment by examining whether records exist, whether the taxpayer cooperated during examination, and whether the same underreporting appears year after year. A single missed income source might indicate carelessness; consistent omission across multiple years signals intent to defraud.

False Charitable Donations and Fabricated Credits

False charitable donations and fabricated credits create another avenue for fraud that leaves documentary evidence behind. Taxpayers claim donations to nonexistent charities, overstate the value of donated property, or claim education credits for dependents who never attended school. The IRS catches these schemes through cross-referencing charity registrations, requesting appraisals, and verifying enrollment records.

The documentation trail exposes these claims quickly. Someone claiming $50,000 in charitable donations without receipts or claiming education credits for a dependent who attended no accredited institution invites immediate scrutiny. The IRS maintains databases of legitimate charities and educational institutions, making false claims easy to identify.

Business Loss Fabrication and Inflated Expenses

Business loss fabrication works through similar mechanisms. Fraudsters create fake expenses, claim losses from nonexistent business ventures, or shift legitimate losses to inflated amounts. Someone claiming $200,000 in business losses when their actual business generated only $50,000 in expenses invites immediate scrutiny. False documents, altered invoices, and missing supporting records all strengthen the IRS’s case and lead to penalties for underpayments.

The Intent Standard That Separates Fraud from Error

The standard for proving civil fraud requires clear and convincing evidence, meaning the IRS doesn’t need criminal-level proof but does need documentation showing intentional misstatement. The key distinction separates honest mistakes from deliberate deception: did the taxpayer maintain records, attempt to justify positions, and cooperate with the IRS, or did they destroy documents, make false statements, and obstruct examination? Taxpayers who maintain poor records, refuse to provide documentation, and show patterns of concealment across years face fraud penalties that dwarf accuracy-related penalties. The IRS applies accuracy-related penalties of 20% to underpayments when negligence or disregard of rules is demonstrated, making the difference between a careless error and deliberate fraud extraordinarily significant for your tax liability.

How the IRS Actually Catches Tax Fraud

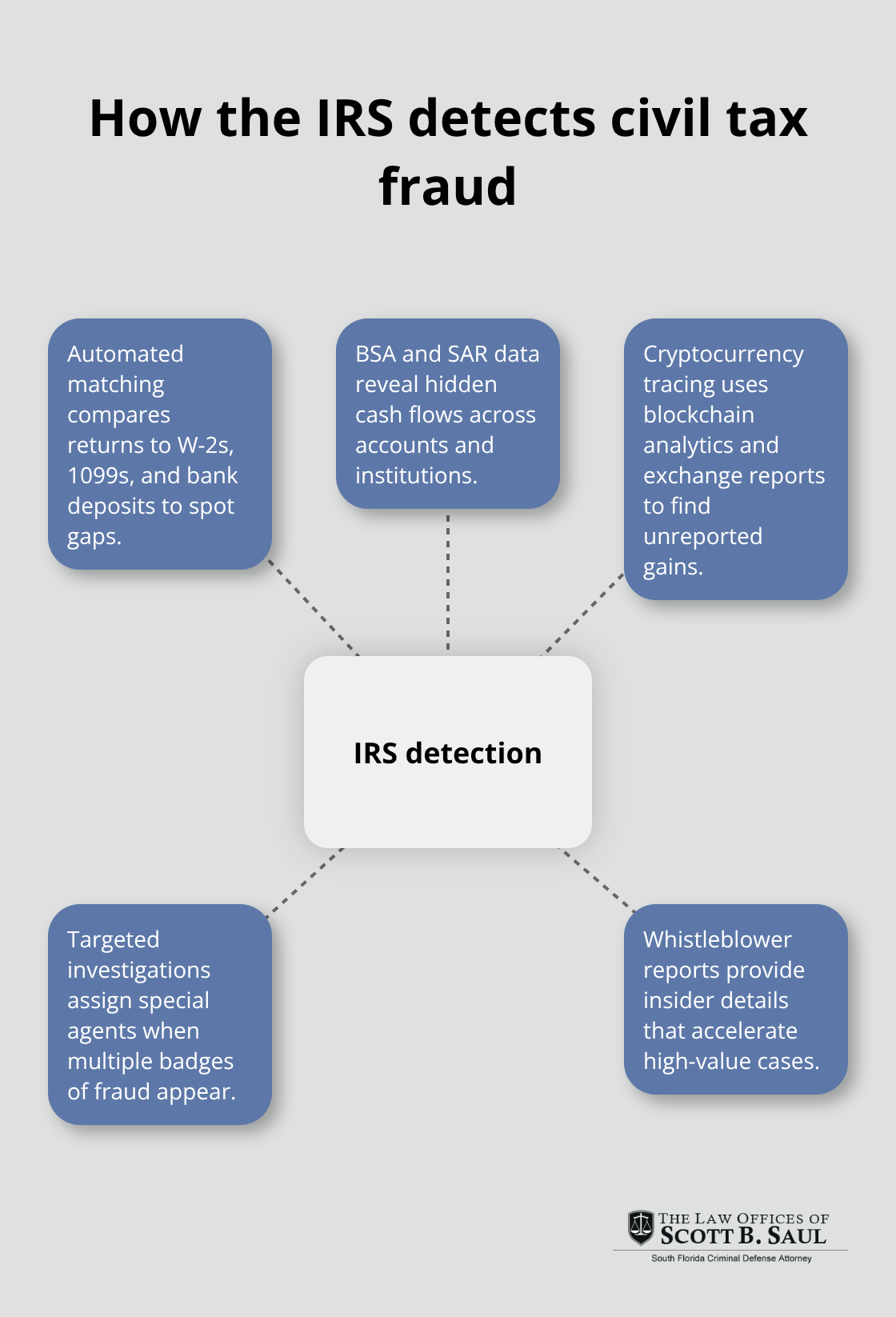

The IRS deployed sophisticated technology long before most businesses modernized their systems. The agency’s automated matching systems cross-reference income reported on tax returns against third-party documents like W-2s, 1099s, and bank deposit records filed separately by employers and financial institutions. When your return shows $50,000 in income but your bank statements reveal $120,000 in deposits, the system flags the discrepancy immediately.

Automated Systems and Financial Data Analysis

The IRS Criminal Investigation division processed cases involving Bank Secrecy Act reports, uncovering significant tax fraud through financial data analysis. About 87% of criminal investigations involved a SAR, demonstrating that financial data serves as the primary detection mechanism. The IRS doesn’t rely on guesswork or hunches anymore. Their data analytics systems compare your reported income against industry benchmarks for your profession, cross-check deduction amounts against IRS statistical norms, and identify patterns across multiple years of returns.

Someone claiming $300,000 in home office deductions while operating a consulting business generating $400,000 in revenue triggers immediate algorithmic review. The system also monitors cryptocurrency transactions now, following IRS Notice 2014-21 and subsequent guidance that made digital asset reporting mandatory. Unreported wallet transfers, wash trading, and misreported gains are caught through blockchain analysis and exchange reporting requirements implemented in 2024.

Targeted Investigations and Special Agent Assignment

Targeted investigations follow when automated systems identify suspicious patterns. The IRS assigns special agents to cases involving multiple badges of fraud rather than pursuing every minor discrepancy. Offshore accounts not reported on FBAR or FATCA filings, sudden asset transfers before audits begin, and evidence of destroyed records all qualify for criminal investigation rather than routine civil examination.

Whistleblower Reports and Informant Tips

Whistleblower reports accelerate this process significantly. The IRS Whistleblower Office reviewed submissions from informants who identified specific fraud schemes, and these reports led to criminal prosecutions in high-value cases. Someone reporting that their employer systematically pays workers in cash while claiming full payroll deductions can trigger an investigation that exposes pyramiding schemes and trust fund tax violations.

The agency pays rewards ranging from 15% to 30% of collected taxes when whistleblower information leads to successful prosecution. This financial incentive means competitors, disgruntled employees, and business partners actively report suspected fraud. Your confidentiality is protected under IRC Section 7623, meaning the whistleblower’s identity remains sealed. The conviction rate for cases developed through criminal investigation reaches 97.3%, with average sentences around 37 months, indicating that prosecutions pursued through this channel involve substantial evidence and deliberate intent rather than technical violations.

Final Thoughts

Civil tax fraud indicators cluster around three core areas: income inconsistencies, deduction fabrication, and asset concealment. The IRS identifies these patterns through automated systems that cross-reference your reported income against bank deposits, third-party documents, and industry benchmarks. When your lifestyle exceeds your reported earnings, when deductions far exceed industry norms, or when assets suddenly move before an audit begins, investigators take notice.

Accurate reporting and thorough documentation protect you far more effectively than any concealment strategy. The IRS processes Bank Secrecy Act reports that reveal financial activity you might assume stays private, and their data analytics systems catch discrepancies automatically. Maintaining consistent records, reporting all income sources, and substantiating deductions with receipts and documentation removes the appearance of intent that triggers civil tax fraud investigations.

If you face fraud allegations, experienced legal representation becomes essential immediately. Law Offices of Scott B. Saul provides aggressive representation when tax fraud allegations threaten your freedom and finances, with locations in Miami-Dade and Broward County.

Archives

- February 2026 (5)

- January 2026 (9)

- December 2025 (9)

- November 2025 (8)

- October 2025 (8)

- September 2025 (9)

- August 2025 (8)

- July 2025 (8)

- June 2025 (9)

- May 2025 (9)

- April 2025 (8)

- March 2025 (9)

- February 2025 (8)

- January 2025 (9)

- December 2024 (10)

- November 2024 (5)

- July 2024 (2)

- June 2024 (2)

- May 2024 (2)

- April 2024 (2)

- March 2024 (2)

- February 2024 (2)

- January 2024 (2)

- December 2023 (2)

- November 2023 (2)

- October 2023 (2)

- September 2023 (2)

- August 2023 (1)

- July 2023 (2)

- June 2023 (2)

- May 2023 (2)

- April 2023 (2)

- March 2023 (2)

- February 2023 (2)

- January 2023 (2)

- December 2022 (2)

- November 2022 (2)

- October 2022 (2)

- September 2022 (2)

- August 2022 (2)

- July 2022 (2)

- June 2022 (2)

- May 2022 (2)

- April 2022 (2)

- March 2022 (2)

- February 2022 (2)

- January 2022 (2)

- December 2021 (2)

- November 2021 (2)

- October 2021 (2)

- September 2021 (2)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (2)

- April 2021 (2)

- September 2020 (5)

- July 2020 (4)

- June 2020 (4)

- May 2020 (4)

- April 2020 (5)

- March 2020 (4)

- February 2020 (4)

- January 2020 (4)

- December 2019 (1)

- November 2019 (4)

- October 2019 (4)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (4)

- April 2019 (4)

- March 2019 (4)

- February 2019 (4)

- January 2019 (4)

- December 2018 (4)

- November 2018 (5)

- October 2018 (5)

- September 2018 (4)

- August 2018 (4)

- July 2018 (7)

- June 2018 (4)

- May 2018 (4)

- April 2018 (8)

- March 2018 (4)

- February 2018 (4)

- January 2018 (4)

- November 2017 (4)

- October 2017 (4)

- September 2017 (4)

- August 2017 (7)

- July 2017 (6)

- June 2017 (4)

- May 2017 (4)

- April 2017 (4)

- March 2017 (4)

- February 2017 (7)

- January 2017 (4)

- December 2016 (7)

- November 2016 (4)

- October 2016 (4)

- September 2016 (10)

- August 2016 (4)

- July 2016 (4)

- June 2016 (4)

- May 2016 (4)

- April 2016 (4)

- March 2016 (4)

- February 2016 (7)

- January 2016 (4)

- December 2015 (5)

- November 2015 (4)

- October 2015 (7)

- September 2015 (4)

- August 2015 (4)

- July 2015 (13)

- June 2015 (9)

- May 2015 (8)

- April 2015 (6)

- March 2015 (4)

- February 2015 (4)

- January 2015 (4)

- December 2014 (4)

- November 2014 (4)

- October 2014 (4)

- September 2014 (3)

Categories

- Adjudication (1)

- Bankruptcy (1)

- Burglary Crimes (3)

- calendar call (1)

- Car Accident (1)

- Criminal Defense (395)

- Cyber Crimes (7)

- DNA (1)

- Domestic Violence (9)

- Drug Crimes (5)

- DUI (12)

- Embezzlement (1)

- Environmental Crimes (4)

- Expungement Law (2)

- Federal Sentencing Law (3)

- Firearm (3)

- Forgery (4)

- General (82)

- Healthcare (3)

- Immigration (1)

- Indentity Theft (1)

- Insurance (5)

- judicial sounding (2)

- Juvenile Crimes (4)

- Manslaughter (4)

- Money Laundering (3)

- Organized Crime (1)

- Racketeering (1)

- Reckless Driving (3)

- RICO (3)

- Sealing and Expunging (2)

- Sex Offense (1)

- Shoplifting (1)

- Suspended Driver's License (1)

- Traffic (4)

- Trending Topics (1)

- White-collar Offenses (1)