Tax Fraud Sentencing Guidelines Overview

By : saulcrim | Category : Criminal Defense | Comments Off on Tax Fraud Sentencing Guidelines Overview

12th Jan 2026

Tax fraud carries serious consequences that can reshape your life. Understanding tax fraud sentencing guidelines is essential if you’re facing charges or want to protect yourself from prosecution.

We at Law Offices of Scott B. Saul have guided clients through federal and state tax cases for years. This guide breaks down how courts determine sentences, what penalties you might face, and why legal representation matters.

How Courts Distinguish Between Tax Crimes

The IRS distinguishes between tax crimes in ways that directly affect your sentencing. Willfulness and the dollar amount involved determine whether you face a felony or misdemeanor charge. Tax evasion under 26 U.S.C. § 7201 carries up to 5 years in prison and fines up to $100,000 for individuals or $500,000 for corporations. Willful failure to file or pay taxes under 26 U.S.C. § 7203 results in up to 1 year in prison, while filing a fraudulent return under 26 U.S.C. § 7206 can bring up to 3 years. Prosecutors must prove willfulness-an affirmative, voluntary act to evade or defeat a tax. Honest mistakes on your return don’t meet this threshold, but intentional underreporting or deliberate concealment does.

The Real Sentencing Picture

Federal data from FY2024 shows that 66% of tax fraud defendants received prison sentences, with an average of 15 months served. The median tax loss for these cases reached $491,302, though 20.5% involved losses exceeding $1.5 million. Prison time represents only part of the penalty. Civil fraud penalties impose a penalty on the additional tax due, plus interest that accrues indefinitely. A $500,000 underreported tax liability becomes a significantly larger civil debt before criminal penalties apply.

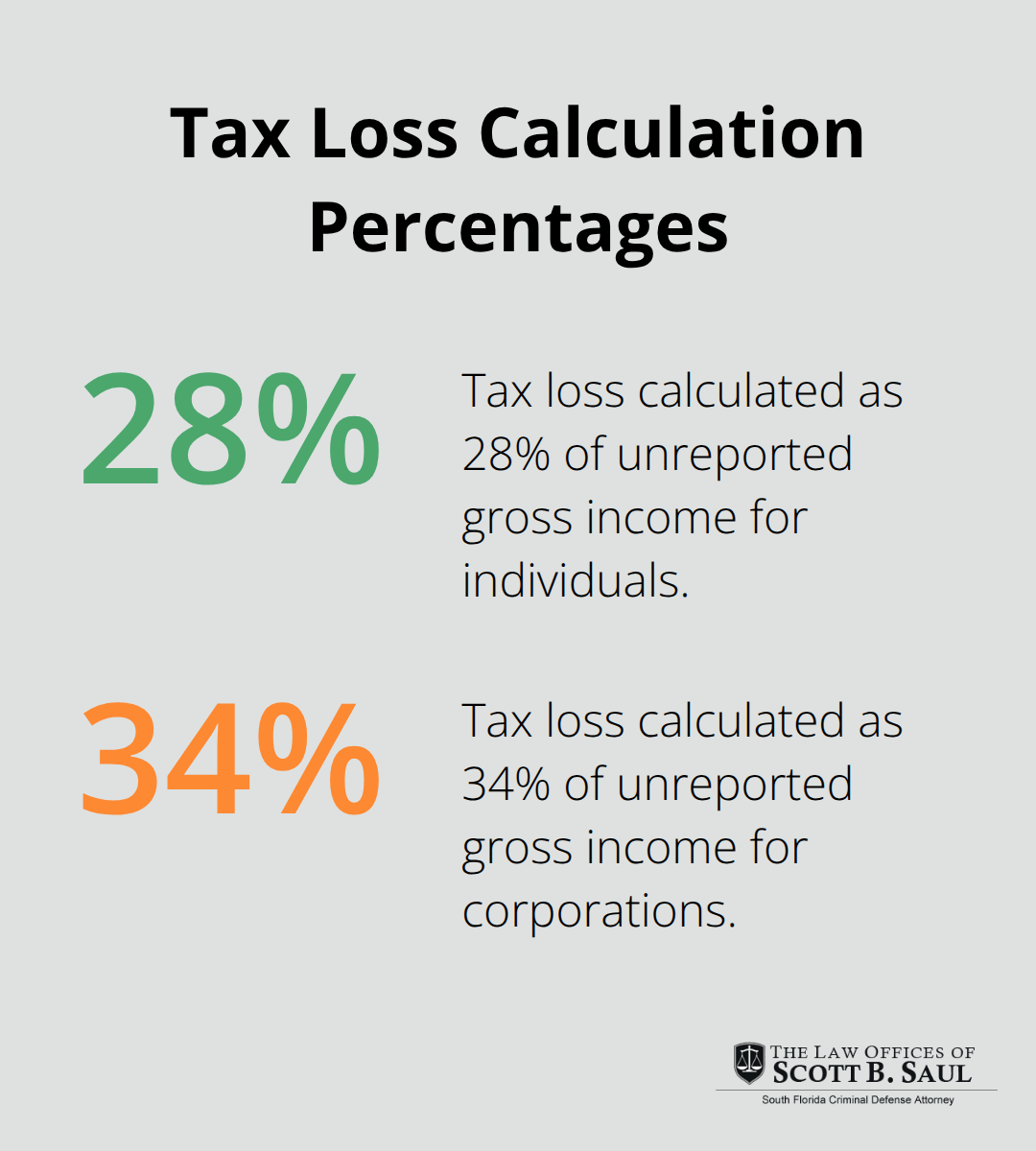

How the Tax Loss Table Works

Federal sentencing guidelines use a Tax Loss Table that translates your underreported income into a base offense level. The calculation follows a clear formula: 28% of unreported gross income for individuals, or 34% for corporations. A $520,000 tax loss yields Base Offense Level 18. This table forms the foundation for your sentence, but specific factors then enhance it significantly.

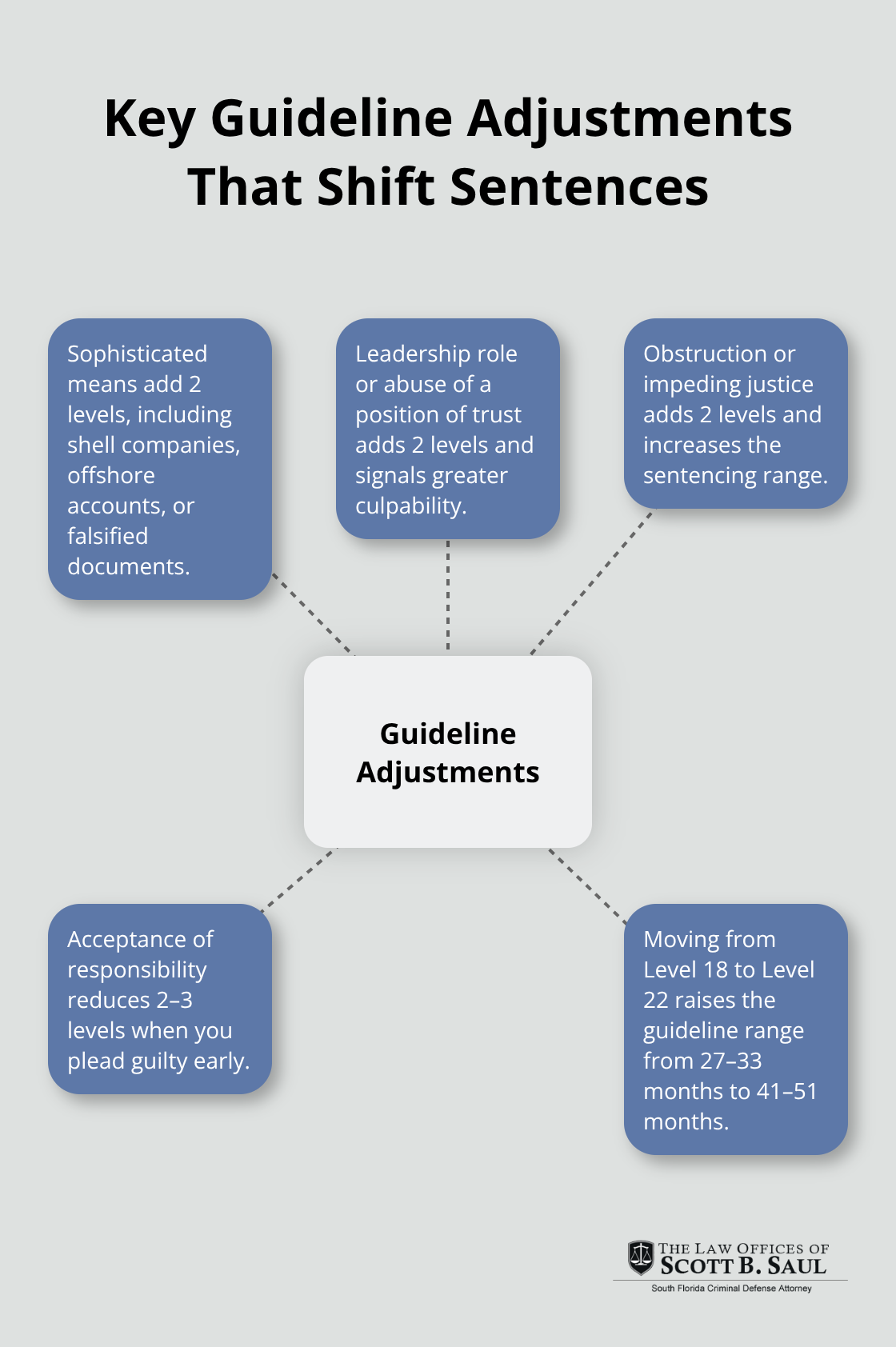

Enhancements That Increase Your Sentence

Specific circumstances add points to your offense level. The guidelines add 2 points if your scheme involved sophisticated means-such as shell companies, offshore accounts, or falsified documents. An additional 2 points apply if you held a leadership role or abused a position of trust. Federal data confirms this matters: 16.9% of sentenced defendants faced enhancements for sophisticated means, while 6.5% faced them for obstruction or impeding justice.

How Cooperation Reduces Your Sentence

Acceptance of responsibility through a guilty plea reduces your offense level by 2–3 points, potentially shortening your sentence by months. First-time offenders with minimal prior criminal history (86.8% of tax fraud defendants according to FY2024 data) experience downward variances in over half of cases, with average sentence reductions of 64.4%. Cooperation and early legal intervention produce substantially better outcomes than hoping for leniency at sentencing.

The specific enhancements and reductions available to you depend on the facts of your case and how prosecutors present them. Understanding these mechanisms helps you evaluate your options before trial.

How Sentencing Guidelines Calculate Your Offense Level

The federal sentencing framework transforms your tax loss into a precise offense level that determines your prison range. The U.S. Sentencing Commission guidelines use the Tax Loss Table, which maps dollar amounts directly to base offense levels ranging from Level 6 to Level 26. For a $520,000 tax loss, you start at Level 18. This isn’t theoretical-it’s the mechanical foundation that prosecutors and judges use to recommend and impose sentences. The calculation method is standardized: 28% of unreported gross income for individuals or 34% for corporations, plus 100% of any false credits you claimed. If you underreported $1.86 million in income, the IRS calculates your tax loss at roughly $520,000, landing you at Level 18 before any adjustments. Tax loss includes intended loss, not just actual loss-even unsuccessful evasion schemes count. This means prosecutors don’t need to prove you actually got away with it; they prove what you tried to hide.

Adjustments That Shift Your Sentence Range

After establishing your base level, specific offense characteristics add or subtract points. Sophisticated means-shell companies, offshore accounts, falsified documents, or complex layering schemes-add 2 levels. If you held a supervisory role or abused a position of trust, another 2 levels apply. Obstruction or impeding justice adds 2 more levels. These adjustments produce real consequences; moving from Level 18 to Level 22 shifts your guideline range from 27–33 months to 41–51 months. The defendant bears the burden to prove legitimate unclaimed deductions that might reduce tax loss, making early documentation critical. Acceptance of responsibility through a guilty plea reduces your level by 2–3 points.

First-time offenders with no prior record experience downward variances in many cases, with average reductions of 64.4 months.

How Cooperation Changes Your Outcome

Early cooperation with prosecutors produces substantially better results than fighting charges through trial. Guilty pleas reduce your offense level by 2–3 points, potentially shortening your sentence by months. Substantial assistance departures (cooperation with the government) yield significant sentence reductions. The difference between fighting and cooperating early is substantial. Judges rarely sentence above guidelines in tax cases, but they frequently sentence below them when defendants cooperate. This discretion under 18 U.S.C. § 3553(a) rewards those who take responsibility early rather than forcing the government to prove its case at trial.

What Mandatory Minimums Actually Mean

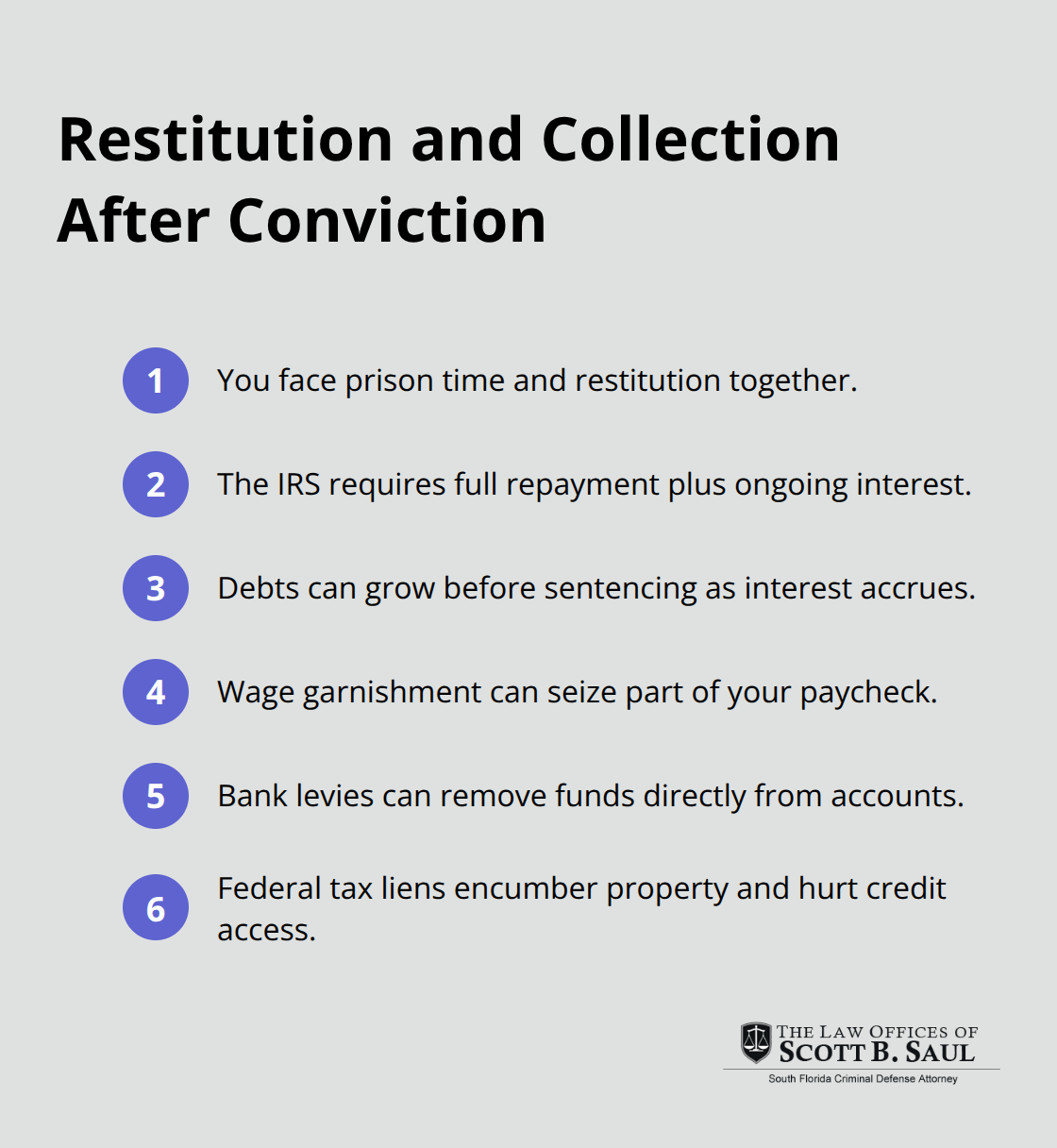

Federal tax crimes carry no mandatory minimum prison sentences, contrary to common assumptions. Tax evasion under 26 U.S.C. § 7201 has a statutory maximum of 5 years; fraudulent returns under § 7206 max out at 3 years; willful failure to file under § 7203 maxes at 1 year. The sentencing guidelines are advisory, not mandatory, since Booker v. United States. However, restitution to the IRS for the full tax loss is typically required in addition to any prison term. A Level 22 defendant might serve 41–51 months and still owe $500,000 or more in restitution. The combination of prison time and financial restitution-not a choice between them-creates the true financial and personal impact of a tax conviction. Your criminal history category combines with your adjusted offense level to determine your final sentencing range on the Sentencing Table, which means your prior record directly influences how harshly judges treat your current offense.

What Actually Happens After a Tax Conviction

Prison time for tax fraud varies dramatically based on tax loss and criminal history. Federal data from FY2024 shows the average sentence was 15 months, but this masks the real range. Defendants with tax losses under $100,000 typically serve shorter terms, while those exceeding $1.5 million face substantially longer sentences. A Level 18 offense (around $520,000 tax loss) produces a guideline range of 27–33 months for a first-time offender, but judges sentence below guidelines in 45.2% of cases.

How Criminal History Determines Your Sentence Range

The Criminal History Category matters enormously in tax sentencing. A defendant with no prior record falls into Category I, while prior convictions push you into Category IV, V, or VI with dramatically higher ranges. Federal data reveals that 86.8% of tax fraud defendants had little or no prior criminal history, yet their sentences still reflected the severity of the offense. Your prior record directly influences how harshly judges treat your current offense when combined with your adjusted offense level on the Sentencing Table.

The Real Cost: Restitution and Financial Obligations

Restitution complicates the picture significantly because you don’t choose between prison time and restitution-you face both. The IRS demands full repayment of the tax loss, plus interest that continues accruing. A $500,000 tax loss becomes $600,000 or more by the time sentencing occurs. This financial obligation follows you for years, with wage garnishment, bank levies, and federal tax liens becoming enforcement tools. The IRS collected substantial amounts in unpaid assessments, demonstrating aggressive collection practices.

Professional Licenses and Career Destruction

A tax conviction destroys professional credentials and financial stability in ways that extend far beyond incarceration. The conviction itself triggers collateral consequences that prosecutors rarely mention during plea negotiations. Your professional licenses may be revoked or denied, limiting career options in fields like accounting, law, medicine, and real estate. Federal employment becomes permanently unavailable. Background checks reveal the conviction indefinitely, eliminating opportunities in banking, insurance, government contracting, and management positions.

Long-Term Financial and Reputational Damage

A 75% civil fraud penalty applies to the additional tax due, plus interest accruing indefinitely, creating a debt that outlasts prison time. The conviction record prevents bonding for certain positions and disqualifies you from holding fiduciary roles. Clients and employers conduct background checks routinely, and a tax conviction appears prominently. Your reputation within professional communities suffers irreversible damage. These collateral consequences often exceed the prison sentence in long-term impact. Fighting charges through trial risks all these consequences plus higher sentences; cooperating early and negotiating a resolution protects your professional future more effectively than hoping for acquittal.

Final Thoughts

Tax fraud sentencing guidelines create predictable outcomes that reshape your financial, professional, and personal life. Federal data shows that 66% of tax fraud defendants receive prison time averaging 15 months, yet 45.2% are sentenced below guidelines when they cooperate early. This disparity reflects a critical reality: your choices before trial determine whether you face the full force of the guidelines or negotiate a substantially better outcome.

Willfulness matters, but so does timing. Prosecutors must prove intentional wrongdoing, not honest mistakes, yet the burden shifts once they establish your scheme. Fighting charges through trial risks maximum sentences, professional license revocation, and permanent career damage. Accepting responsibility through early cooperation produces downward variances averaging 64.4 months and protects your future more effectively than hoping for acquittal.

Legal representation in tax cases is not optional. The difference between representing yourself and working with an experienced tax defense attorney is the difference between facing 41–51 months in prison versus 21–27 months, or between losing your professional license and preserving your career. An attorney challenges tax loss calculations, identifies legitimate deductions prosecutors overlook, and negotiates plea agreements that minimize collateral consequences. If you face tax fraud allegations or investigation, contact our criminal defense team in South Florida immediately, as early intervention changes outcomes dramatically.

Archives

- February 2026 (5)

- January 2026 (9)

- December 2025 (9)

- November 2025 (8)

- October 2025 (8)

- September 2025 (9)

- August 2025 (8)

- July 2025 (8)

- June 2025 (9)

- May 2025 (9)

- April 2025 (8)

- March 2025 (9)

- February 2025 (8)

- January 2025 (9)

- December 2024 (10)

- November 2024 (5)

- July 2024 (2)

- June 2024 (2)

- May 2024 (2)

- April 2024 (2)

- March 2024 (2)

- February 2024 (2)

- January 2024 (2)

- December 2023 (2)

- November 2023 (2)

- October 2023 (2)

- September 2023 (2)

- August 2023 (1)

- July 2023 (2)

- June 2023 (2)

- May 2023 (2)

- April 2023 (2)

- March 2023 (2)

- February 2023 (2)

- January 2023 (2)

- December 2022 (2)

- November 2022 (2)

- October 2022 (2)

- September 2022 (2)

- August 2022 (2)

- July 2022 (2)

- June 2022 (2)

- May 2022 (2)

- April 2022 (2)

- March 2022 (2)

- February 2022 (2)

- January 2022 (2)

- December 2021 (2)

- November 2021 (2)

- October 2021 (2)

- September 2021 (2)

- August 2021 (2)

- July 2021 (2)

- June 2021 (2)

- May 2021 (2)

- April 2021 (2)

- September 2020 (5)

- July 2020 (4)

- June 2020 (4)

- May 2020 (4)

- April 2020 (5)

- March 2020 (4)

- February 2020 (4)

- January 2020 (4)

- December 2019 (1)

- November 2019 (4)

- October 2019 (4)

- September 2019 (4)

- August 2019 (4)

- July 2019 (5)

- June 2019 (4)

- May 2019 (4)

- April 2019 (4)

- March 2019 (4)

- February 2019 (4)

- January 2019 (4)

- December 2018 (4)

- November 2018 (5)

- October 2018 (5)

- September 2018 (4)

- August 2018 (4)

- July 2018 (7)

- June 2018 (4)

- May 2018 (4)

- April 2018 (8)

- March 2018 (4)

- February 2018 (4)

- January 2018 (4)

- November 2017 (4)

- October 2017 (4)

- September 2017 (4)

- August 2017 (7)

- July 2017 (6)

- June 2017 (4)

- May 2017 (4)

- April 2017 (4)

- March 2017 (4)

- February 2017 (7)

- January 2017 (4)

- December 2016 (7)

- November 2016 (4)

- October 2016 (4)

- September 2016 (10)

- August 2016 (4)

- July 2016 (4)

- June 2016 (4)

- May 2016 (4)

- April 2016 (4)

- March 2016 (4)

- February 2016 (7)

- January 2016 (4)

- December 2015 (5)

- November 2015 (4)

- October 2015 (7)

- September 2015 (4)

- August 2015 (4)

- July 2015 (13)

- June 2015 (9)

- May 2015 (8)

- April 2015 (6)

- March 2015 (4)

- February 2015 (4)

- January 2015 (4)

- December 2014 (4)

- November 2014 (4)

- October 2014 (4)

- September 2014 (3)

Categories

- Adjudication (1)

- Bankruptcy (1)

- Burglary Crimes (3)

- calendar call (1)

- Car Accident (1)

- Criminal Defense (395)

- Cyber Crimes (7)

- DNA (1)

- Domestic Violence (9)

- Drug Crimes (5)

- DUI (12)

- Embezzlement (1)

- Environmental Crimes (4)

- Expungement Law (2)

- Federal Sentencing Law (3)

- Firearm (3)

- Forgery (4)

- General (82)

- Healthcare (3)

- Immigration (1)

- Indentity Theft (1)

- Insurance (5)

- judicial sounding (2)

- Juvenile Crimes (4)

- Manslaughter (4)

- Money Laundering (3)

- Organized Crime (1)

- Racketeering (1)

- Reckless Driving (3)

- RICO (3)

- Sealing and Expunging (2)

- Sex Offense (1)

- Shoplifting (1)

- Suspended Driver's License (1)

- Traffic (4)

- Trending Topics (1)

- White-collar Offenses (1)